Privacy MCP is a new integration that connects your Privacy account to AI assistants like Claude and ChatGPT. With it, you can create cards, pause and close cards, and track spending directly from your AI tools.

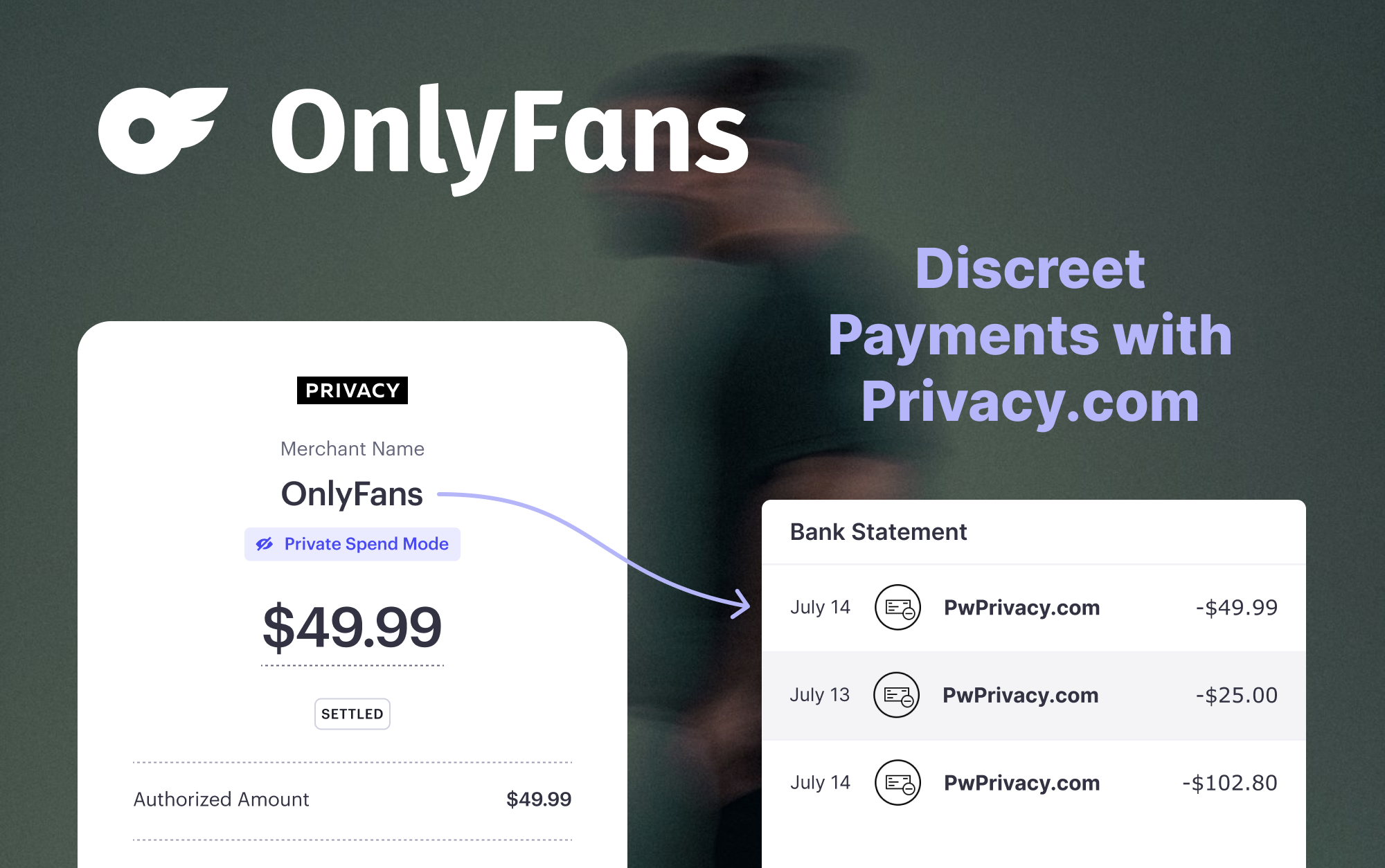

OnlyFans charges show up as "ONLYFANS.COM" on your bank statement. Privacy's Private Spend Mode hides the merchant name entirely—your statement only shows "PWP*Privacy.com." Here's how to set it up.

This guide covers how to use the Privacy API to create virtual cards, set spending limits, monitor transactions, and manage card state programmatically within an agentic workflow.

OpenClaw is one of the most capable AI agents available today, but giving it access to your financial accounts and systems carries real risk. Before providing any payment method or other sensitive information to an autonomous agent, it’s worth understanding what can go wrong and how to protect yourself.

AI agents are no longer just answering questions—they’re spending money. Tools like OpenClaw are booking flights, purchasing domains, paying for API access, and buying groceries, all without human intervention at checkout. However, the challenge AI builders are facing is how to give them spending power safely.

Learn how to safely give AI agents like OpenClaw spending power. Virtual cards with spend limits let you experiment with agentic payments with less risk.

Passkeys are an authentication method used to log into websites and apps with just your fingerprint, face, or PIN. They're more secure than passwords and typically easier to use.

Discover practical ways to prevent ransomware on your computer and smartphone, and learn how virtual cards secure your financial info and reduce payment risks.

Learn how to protect passwords from hackers and reduce your risk of account compromise. Explore the best practices to keep your finances safe online.

Can chip credit cards be hacked despite EMV security? Discover common threats and vulnerabilities and secure your payments with comprehensive protection.

Discover what to do if your credit card is hacked to limit the damage. Learn how to report card fraud, protect your accounts, and prevent future attacks.

Phishing prevention isn’t just about awareness—it’s about damage control. Learn how to avoid common scams and how virtual cards protect you when scams succeed.